Contributors: Fiona Buchanan, Neil Campbell

Date published: 6 June 2023

Securitisation in Scotland – Q&A

Introduction

Shepherd and Wedderburn has been at the forefront of securitisation in Scotland since the first structures were developed and put in place by our lawyers over 30 years ago. Since then, as the market has matured, our team has continued to grow and develop to maintain our position as the pre-eminent securitisation team in Scotland.

This Q&A looks at some of the most common questions we encounter when a participant in the securitisation market is embarking on a transaction where the securitised pool includes Scottish assets. Although the main focus of this Q&A is a basic securitisation structure, most of the Scottish general principles will be applicable across different types of transactions, from mortgage warehousing to covered bond and master trust structures.

Why do we need Scottish legal advice?

Although the Scottish legal system shares much in common with England and Wales, Scotland has its own distinct legal system and there are some key differences which impact how Scottish assets are securitised.

Transfer and sale

One key difference is that Scots law does not have a concept of equity in the same way as England and Wales. This has an impact on how certain rights are created, held and transferred. In England, there is a distinction between the legal and equitable title to assets whereas in Scotland there is no such distinction between legal and equitable title (only legal title). To create a structure as close as possible to the transfer of equitable title under the sale agreement, and to support true sale analysis, the legal title holder declares a Scots law-governed trust in favour of the issuer over any Scottish assets. This gives the issuer all the rights and protections of a beneficiary under a trust. The assets held in the trust are removed from the patrimony of the legal title holder and would not be available to its creditors in an insolvency scenario. Unlike a transfer of legal title, notification to underlying borrowers/customers/consumers of the trust is not required.

Security

The absence of equity also affects how security is created. Whilst in England, the issuer will typically grant a security package over its assets, comprised of fixed charges or security assignments under the English deed of charge, in Scotland, fixed security is granted by way of assignation in security of the issuer’s beneficial interest under the Scottish trust.

Future assets

Another key difference relates to how future assets are treated, for example, assets which have not been originated at closing, but which are to be sold into the structure in future. In Scotland, it is not possible to transfer, create a trust or create fixed security over assets that do not exist at the time of the transfer, trust or fixed security. This means that when future assets are sold into the securitised pool after closing, they will not automatically fall within the existing Scottish trust or security and will not form part of the issuer’s assets. In this case, a supplemental trust and supplemental assignation in security must be entered into.

Legal title transfers

Finally, the method by which legal title to assets is transferred is different in Scotland. For a securitised pool comprising residential or commercial mortgages, a statutory form of assignation is required (under the Conveyancing and Feudal Reform (Scotland) Act 1970) which is different to the English equivalent, and which must be registered at Registers of Scotland. For other receivables, a Scots law-compliant assignation is required which must be notified to the underlying borrowers/counterparties in order to be effective.

What Scottish documents are typically used in a securitisation deal?

Typically, Scottish documents on any securitisation transaction fall into two categories: (A) those that are required at closing to effect the trust and security interests mentioned above and (B) those that are only required to effect a legal title transfer and further security over those interests upon a perfection or other trigger event occurring.

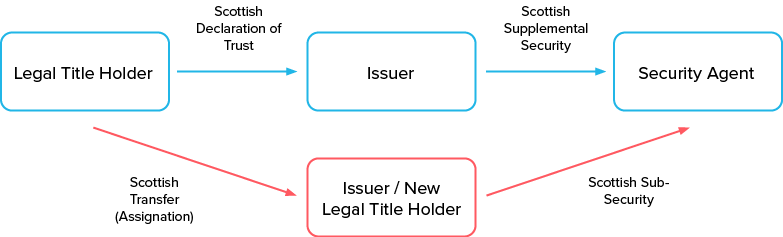

In relation to the first category (A), the principal Scottish documents are typically the Scottish declaration of trust and the Scottish supplemental security.

The Scottish declaration of trust will be granted by the legal title holder in favour of the issuer, both of which are party to the document. There may be other parties to the trust depending upon the structure of the transaction.

Under Scots law, the assets held in trust must be objectively identifiable and so the detail of the assets being held in trust must meet a certain minimum threshold. For land-related deals (including residential and commercial mortgages) this means that a schedule of mortgage data must be appended to the trust and signed by the parties. The quality of data will vary depending on the lender/servicer’s operating systems but, in general, the data should at least include account numbers, secured property addresses and title numbers in order to meet Scots law requirements. In other cases, borrower names and secured sums outstanding may also have to be included.

The form of Scottish declaration of trust will customarily be scheduled to the sale agreement and there will be an obligation on the legal title holder to enter into the trust at closing. Where future sales into the securitised pool are anticipated, the sale agreement will also contain a mechanism for future Scots law declarations of trust to be entered into.

The Scottish supplemental security (sometimes known as the Scottish supplemental charge or Scottish trust security) is a security document under which the issuer grants an assignation in security of its interest in the Scottish trust in favour of the security trustee. It is broadly equivalent to the fixed charge contained in the English deed of charge granted over the equitable interest in any English assets.

The form of Scottish supplemental security will customarily be scheduled to the English deed of charge and there will be an obligation in the English deed of charge on the issuer to enter into it at closing. Where future sales into the securitised pool are anticipated, the English deed of charge will usually contain a mechanism for further Scottish supplemental securities to be entered into. The assignation in security must be perfected by notification to the legal title holder and this will normally be achieved by having the legal title holder join as a party to the Scottish supplemental security.

In relation to the second category (B), the Scottish transfer is an assignation to effect the transfer of legal title from the legal title holder to the issuer in the event that a perfection event under the sale agreement occurs. For land-related deals, this follows a statutory form set out in the Conveyancing and Feudal Reform (Scotland) Act 1970 and will customarily be scheduled to the sale agreement. In the event that such Scottish transfers are entered into, these would require to be registered at Registers of Scotland. For non-land transactions, an assignation of the relevant receivables would be required to transfer legal title to the assets. This would have to be perfected by notice to the underlying borrowers/counterparties.

The Scottish sub-security is a security document whereby the issuer grants fixed security over its legal title to any Scottish mortgages in the securitised pool. This follows a statutory form of standard security and will customarily be scheduled to the English deed of charge, with obligations to grant such fixed security contained within the English deed of charge. In the event that such Scottish sub-securities are entered into, these would require to be registered in the Scottish land register and as a charge at Companies House. Scottish sub-securities are more commonly granted on land-related securitisation transactions. Other types of fixed security, such as an assignation in security of receivables under Scottish contracts, would be required in respect of other non-land assets.

Finally, depending on the nature of the transaction, additional Scots law documents may be required within the structure. Where the underlying receivables are tied to an asset that may have residual value (such as vehicles or equipment), an additional Scots law asset declaration of trust or Scots law asset floating charge would typically be granted in respect of these assets to capture such residual value. Separately, where a securitisation structure – including Scots law trust(s) – is already in place but the legal title holder is changing, a Scottish deed of assumption and resignation would be required to replace the outgoing legal title holder with the incoming legal title holder in relation to the Scottish trusts.

Are there any other transaction or listing documents relevant to Scotland?

Yes. In addition to the Scottish documents referred to above, certain English transaction documents have particular relevance to the Scottish aspects of any securitisation.

The sale agreement will usually be expressly governed by English law and the Scottish courts will (except in certain “Rome 1” circumstances) give effect to the parties’ choice of English law. Where a sale agreement includes Scottish assets, parties will usually want to ensure that input is provided from a Scottish perspective. This is to ensure that, for example, any warranties given are appropriately tailored for Scottish assets and that any mechanism for the execution and delivery of a Scottish trust is provided for. Perfection event triggers and deliverables will also be reviewed so that in the event of legal title transfers being required, the Scottish equivalents will be included.

The English deed of charge will in most cases contain a floating charge, which should be drafted so that it covers the issuer’s assets in Scotland. The English deed of charge will also be appropriately tailored to provide for the delivery of the Scottish security documents and the inclusion of certain Scottish-related enforcement language.

The servicing agreement, subscription agreement, trust deed and any agreement setting out common terms or definitions are usually reviewed from the Scottish perspective.

The prospectus or offering circular will also contain a number of elements around the assets in the securitised pool, risk factors and transaction structure that will require Scottish review and input.

Finally, a number of ancillary documents, including powers of attorney and solvency certificates, will usually benefit from review to ensure Scottish aspects are included where appropriate, where those documents are being opined on.

Is a separate due diligence process required?

Yes, where due diligence is being undertaken in respect of the English assets in the securitised pool, there will usually be an equivalent Scottish due diligence process involving a review of any underlying standard documentation used to originate the assets in Scotland. In some cases, this will also include a review of a sample of the loans being securitised. This will follow an equivalent format to any equivalent English due diligence reporting.

Given the mortgage regulatory regime is largely the same across the UK, the focus of the Scottish due diligence exercise will usually be on non-regulatory aspects. For example, an analysis of any restrictions on the transfer of the underlying contracts will be undertaken. The broad principle here is that contracts can be assigned freely except where the contract provides otherwise. The forms of standard documentation will also be analysed to ensure they meet certain Scottish statutory requirements in respect of security documentation and occupiers’ consents.

Is a separate Scots law legal opinion required?

Yes, on rated deals involving Scottish assets, a Scottish legal opinion is customarily required. This covers Scottish analysis of elements of the transaction including the “true sale” aspects of the transaction, the validity of the Scottish transaction documents and the choice of English law to govern the English transaction documents. It will usually also analyse certain insolvency clawback provisions applicable in Scotland which may be relevant in the circumstances of the particular transaction (which are distinct from and operate differently to the equivalent English law provisions).

Likewise for any deals involving a Scottish entity as originator or seller, a capacity and authority opinion would usually be provided.

What documents require to be executed in accordance with Scots law and what are the rules?

Scottish documents

Those documents governed by Scots law, such as the Scottish declaration of trust and Scottish supplemental security, will require to be executed in accordance with Scottish signing formalities. These are contained in the Requirements of Writing (Scotland) Act 1995. For transactions involving interests in land (including RMBS portfolios), the Scottish trust and security documents entered into at closing will require to be subscribed in wet-ink, unless signatories have a Qualified Electronic Signature or “QES”. QES authentication for specified signatories may be arranged prior to closing, although they are not yet in widespread use for standalone deals.

For deals not involving land (such as credit card or auto loan receivables), Scottish documents signed electronically by a simple or advanced electronic signature will be valid, but not “probative” or “self-proving”. This means that they will not benefit from a statutory presumption that the electronic signature is genuine. Additional evidence as to the identity of the signatory and the date and place of signing would likely be needed if the documents were ever brought before a court. A QES is the only type of electronic signature that confers such probative status. In our experience, on the majority of securitisation transactions – particularly where they are rated – parties will therefore sign Scots law transaction documents in wet-ink.

“Subscription” requires that the first signing block appears on the same page as the last piece of operative text of the document. Documents may be executed in advance of closing and may be executed in counterpart under Scots law. The rules on counterpart are similar but not identical to those applicable in England and Wales. It’s also worth noting that the “Mercury” rules don’t apply in Scotland. This means that the full document, including any schedule, should be printed out before being signed, scanned and returned.

Once documents have been signed, the parties or their agents can agree to hold the Scottish documents as undelivered pending closing (this is broadly similar to escrow arrangements under English law). As in England and Wales, it is customary to close transactions on the basis of dated PDF copies of signed documents, albeit the “effective date” of the Scottish documents should be added to the signed documents post-closing. Where documents are executed in wet-ink, this means the effective date being added to the wet-ink originals. After closing, compiled signed and dated versions will be circulated to parties along with any English transaction documentation.

English documents

In some cases where the rating agencies require a particular level of Scottish legal opinion, certain of English transaction documents with particular relevance to the Scottish aspects of the transaction may need to be signed in accordance with both English and Scottish signing requirements. This commonly includes the sale agreement, English deed of charge and deed of release. Signing these documents in accordance with both English and Scottish signing requirements will enable Scots counsel to give certain ratings-level legal opinions in respect of the sale and security aspects of the transaction.

For more detail on the execution of documents in Scotland, see our articles here and here.

Are there any other practicalities to bear in mind?

The Scottish supplemental security will – in the usual way – have to be registered at Companies House within 21 days of its effective date.

What happens when a securitisation is terminated?

Where a securitisation is being refinanced, a call option exercised, or otherwise terminated, there will be a requirement to release the Scottish security and to unwind the Scottish trust in order for the assets to be returned, unencumbered, to the legal title holder. The mechanics of this may in some cases be built into an English deed of release and termination. Alternatively, there may be merit in having a separate Scottish deed of release to which the security holder, the issuer and the legal title holder are a party. Parties should remember to remove charges from the issuer’s charges register after the release and discharge of the Scottish security become effective.

Future reform

On 4 May 2023 the Moveable Transactions (Scotland) Bill was passed by the Scottish Parliament. The Bill simplifies Scots law relating to the assignation of rights and security over moveable property. Once introduced, the Bill will greatly simplify the process for the securitisation of moveable assets (such as credit card or auto loan receivables), including the ability to transfer and create security in respect of future assets. For more information on these major reforms please see our Moveable Transactions landing page.

For any questions about securitisation or other debt capital markets transactions involving Scottish assets, please get in touch with a member of our team.

Contributors:

Fiona Buchanan

Partner and Head of Banking and Finance

Neil Campbell

Director

Further / related posts

28 October 2025

Contributors:

Louisa Knox, Hamish Patrick, Donald Smith, Peter Alderdice

22 October 2025

Joint ventures in the clean energy sector: Transfer conditions

Contributors:

Cameron Kane, John Morrison

24 September 2025

Contributor: Jonathan Carey

To find out more contact us here

Expertise: Banking and Finance, Debt Capital Markets and Securitisation